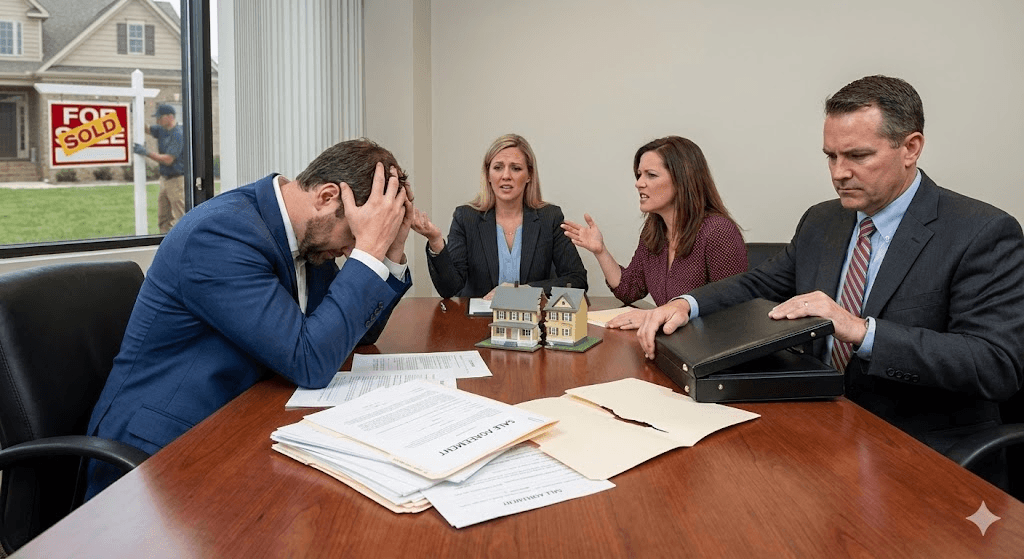

Not long ago, signing a home contract in Venice felt like the hard part. Once the ink was dry, buyers assumed the deal was done. Today, that assumption is quietly unraveling.

Across Florida, a growing number of buyers are backing out of home purchases after contracts are signed, not because they’ve lost interest in owning a home, but because the reality of ownership arrives late — and often with a shock.

According to a recent analysis cited by MSN , contract cancellations are rising as buyers confront costs and risks they didn’t fully grasp when they made their offer.

National data supports the trend. A Redfin report shows that roughly 15% of pending home sales were canceled in mid-2025, one of the highest rates seen in recent years. Tens of thousands of deals never made it to closing — not because buyers vanished, but because something changed between offer and final paperwork.

What’s changing isn’t buyer confidence in Venice, or even the rest of Florida as a place to live. It’s buyer confidence in the numbers. For many, the breaking point comes when estimates turn into invoices. Insurance quotes arrive higher than expected — sometimes dramatically so — or coverage proves harder to secure altogether. HOA documents reveal rising fees, deferred maintenance, or looming special assessments.

Inspection reports surface issues that sellers are unwilling or unable to address. Suddenly, the monthly cost of ownership no longer matches what buyers thought they were agreeing to. This is not “cold feet.” It’s arithmetic.

During Florida’s recent housing boom, buyers moved fast, waived contingencies, and accepted uncertainty as the price of entry. Today’s buyers are doing the opposite. They are slowing down, reading disclosures more closely, and using contingencies as they were intended — as safeguards. When new information changes the risk profile of a home, more buyers are choosing to walk away rather than absorb unknown or escalating costs.

Redfin notes that this behavior is especially visible in states like Florida, and communities like Venice, where insurance volatility and HOA-governed communities are common.

The shift matters because it changes what a signed contract means.

For sellers, an accepted offer is no longer a guarantee. Deals now hinge on transparency, pricing realism, and how well a property holds up under scrutiny. Buyers, meanwhile, are learning that backing out — while emotionally difficult — can be financially prudent if the long-term math doesn’t work.

In communities like Venice, where many homes are newer, deed-restricted, or part of associations, this trend highlights a growing divide between headline prices and lived costs. The sale price may look reasonable. The monthly obligation may not.

The broader takeaway isn’t that Florida’s housing market is collapsing. It’s that buyers are recalibrating. They’re no longer just asking, “Can I buy this house?” They’re asking, “Can I live with it — five years from now, when insurance renews, fees rise, and repairs come due?”

More often than before, the answer is no.

And when that realization arrives late in the process, the contract doesn’t fail at the offer stage. It fails quietly, just before closing — when fear gives way to clarity, and buyers decide that walking away is better than walking in blind.

What would YOU do? If discovering that insurance or HOA costs are much higher after you go under contract, do you walk away — or push through anyway?